Redeeming

Last updated: June 8, 2026

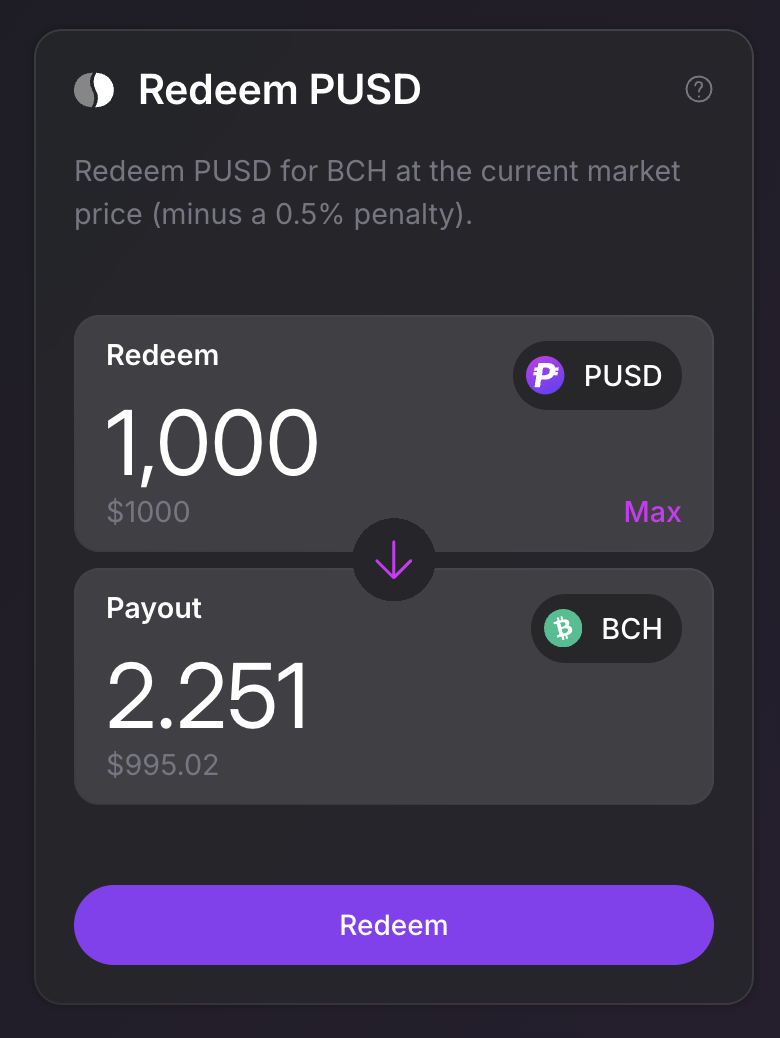

Redeeming lets you exchange PUSD directly for BCH at face value. This mechanism is central to how ParyonUSD maintains its $1 peg: it creates a price floor that prevents PUSD from trading significantly below $1.

Redemptions take a minimum of 12 blocks (about 2 hours) to finalize. If you just want to swap PUSD for BCH, a DEX like Cauldron will usually be faster and cheaper. The main purpose of the redemption mechanism is to enable arbitrage that keeps PUSD pegged to $1.

How redemptions work

- You specify how much PUSD to redeem

- The protocol selects loans to redeem against, starting with the lowest interest rate

- Your PUSD is burned and you receive BCH collateral from those loans

- A 0.5% fee is deducted from the payout, to account for price movement since the last oracle update

Approximate payout = PUSD amount / (BCH price × 1.005)

The exact price is locked in when you create the redemption.

Redemptions are handled entirely on-chain by the smart contracts, with no intermediary. Unlike loans or stakes, a redemption isn’t represented by an NFT you hold or trade; it’s a short-term on-chain process that finalizes automatically.

Why redemptions exist

Redemptions are the primary mechanism that keeps PUSD pegged to $1. Here’s how:

If PUSD trades at $0.98 on the open market, you can buy 100 PUSD for $98 and redeem it for $100 worth of BCH (minus the 0.5% penalty). That’s roughly $1.50 profit per 100 PUSD. This arbitrage opportunity creates buying pressure on PUSD, pushing the price back toward $1.

If PUSD trades at or above $1, there’s no incentive to redeem; you’d be better off selling PUSD on the market directly.

When to prefer a DEX trade

A redemption pays out at the oracle price with a 0.5% premium on the price, and it takes a minimum of 12 blocks to finalize, an uncertain waiting time that can stretch well beyond 2 hours. A DEX trade settles instantly at the market price, with slippage that grows with your trade size. This is why redeeming only pays off when PUSD trades below the peg: at or above $1, a DEX like Cauldron will usually be faster and cheaper. To help you decide, the confirmation dialog shows a live comparison with the current Cauldron rate for the same amount.

Redemptions also have a second-order effect: because the lowest-rate loans are redeemed first, borrowers respond by raising their rates to move back in the queue, so sustained redemption activity pushes overall loan interest rates up. If you have open loans yourself, this is another reason to prefer a DEX trade.

The redemption process

Multiple transactions

Redemptions may require multiple transactions. Each transaction redeems against a single loan, and the protocol can redeem partially against a loan when needed. If your redemption amount exceeds the debt of the first targeted loan, additional transactions are created to redeem against subsequent loans.

The app handles this automatically, showing a multi-step progress view as each transaction processes.

Confirmation time

Each redemption transaction requires 12 block confirmations before it finalizes (approximately 2 hours). During this window, the targeted loan’s collateral is locked but not yet transferred to you.

This confirmation period exists to allow the protocol to verify that the redemption targeted the correct loan (the one with the lowest interest rate). If a lower-rate loan exists, the target can be swapped during this window.

Minimum amount

The minimum redemption amount is 100 PUSD per transaction.

For borrowers: being redeemed against

If you have an active loan, it’s important to understand how redemptions affect you.

How redemptions feel depends on why you opened the loan. Most borrowers want to keep exposure to BCH and use the loan to access dollar liquidity; for them, being redeemed against is an unwanted loss of BCH. See the example and How to protect yourself below. A second, smaller group opens a loan precisely to be redeemed against, as a low-slippage way to convert BCH into PUSD; see Using a 0% loan as a BCH to PUSD conversion tool.

Who gets redeemed first

The protocol always redeems against loans with the lowest interest rates first. What matters is the next-lowest rate across all active loans: as long as your rate is above it, another loan gets redeemed first.

For example, if every other loan pays at least 3%, a 2% loan gets redeemed first, but a 4% loan is safe until the lower-rate loans are exhausted.

One exception: loans with less than 100 PUSD of outstanding debt can be redeemed regardless of interest rate. This lets the protocol clean up sub-minimum-size loans and can happen after a partial redemption leaves a loan just below 100 PUSD.

What happens to your loan

When your loan is redeemed against:

- Your BCH collateral is reduced by the amount of BCH sent to the redeemer.

- Your PUSD debt is reduced by the same dollar amount.

- You keep the borrowed PUSD in your wallet. Redemption only modifies the loan’s debt; it does not touch your wallet balance.

- If only part of your debt is redeemed, your loan key NFT remains valid and the loan stays open with reduced collateral and debt. If the redemption fully repays your debt, the loan is closed and the leftover BCH becomes withdrawable via your loan key.

Interest is only ever charged on outstanding debt, so once part of your loan is redeemed away, you only pay interest on what remains (a fully-redeemed loan accrues no further interest). See How interest works for details.

The 0.5% fee is paid by the redeemer, so you don’t lose in USD terms. The asymmetry is in timing and control: collateral backing a loan stays exposed to BCH price movements and is recoverable any time you repay; BCH that’s been redeemed against you is permanently converted into a debt reduction at the prevailing oracle price, with the timing chosen by the redeemer rather than you.

There is no automatic payout of leftover collateral after a full redemption. Use your loan key to withdraw it.

Example

You have a loan with 1 BCH collateral ($500) and 300 PUSD debt. Someone redeems 100 PUSD against your loan. The on-chain redemption price is 0.5% above the oracle price ($502.50), so approximately 0.199 BCH is extracted:

| Before | After | |

|---|---|---|

| Collateral | 1 BCH ($500) | ~0.801 BCH (~$400.50) |

| Debt | 300 PUSD | 200 PUSD |

| LTV | 60% | ~49.9% |

Your LTV improved, but you lost ~0.199 BCH of collateral. If BCH later rises to $600, that lost collateral would have been worth ~$119.40. The 300 PUSD you borrowed is still in your wallet; only the loan’s debt of record dropped from 300 to 200 PUSD, and you’ll only pay interest on that remaining 200 going forward.

How to protect yourself

- Set a higher interest rate to move further back in the redemption queue.

- Use managed rates to let the protocol automatically adjust your rate based on market conditions.

- Monitor the protocol: if many low-rate loans exist ahead of you, your redemption risk is relatively lower.

See the Borrowing guide for more on interest rate strategy.

While a redemption is pending against your loan

A redemption takes at least 12 blocks to finalize. While one is pending against your loan, the protocol disables some loan actions:

- You cannot withdraw collateral.

- You cannot repay the portion being redeemed. You can still repay debt beyond it, but you cannot close the loan until the redemption finalizes.

- Your loan cannot be liquidated.

These restrictions lift as soon as the redemption finalizes or is cancelled at a period boundary. Adding collateral is still allowed throughout.

Using a 0% loan as a BCH to PUSD conversion tool

You can open a loan precisely so it gets redeemed against, using the protocol as a low-slippage way to convert BCH into PUSD around the oracle price. Set the rate to 0% to sit at the front of the redemption queue.

You don’t control the timing or the price. The redeemer chooses when to redeem, and the conversion happens at whatever the oracle price is at that moment, so you may end up selling into a dip you wouldn’t have chosen yourself. In exchange you avoid the slippage you’d hit moving the same size through a DEX.

A redemption already in progress will not reroute to your new loan. A 0% rate puts you first in line for new redemptions, but a redemption that was already underway when you opened the loan stays on its original target and finalizes there, even if your rate is lower. So higher-rate loans can get redeemed ahead of you, and you wait until a fresh redemption starts before yours is picked up. This is deliberate (see Target loan swaps).

Tradeoffs vs a DEX swap:

- One-time borrowing fees (0.25% protocol + 0.25% front-end) are deducted from your BCH input when the loan is created. This is the main cost of the slow-sell route.

- The 0.5% redemption premium is paid by the redeemer and stays with the loan being redeemed, so unlike a DEX spread it doesn’t come out of your side of the trade. Its primary purpose is to buffer against arbitrage on stale oracle prices.

Risks

Period turnover window

For roughly the last ~2 hours of each daily period (the last 12 blocks of every 144-block period), the redemption interface is disabled. A redemption started inside this window would not finalize before the period ends and would be cancelled by the contract, so this frontend hides the redeem form during the window and shows a notice with the number of blocks until it reopens. The form becomes available again automatically when the next period starts.

Target loan swaps

Your redemption price is locked in at creation and does not change during the confirmation window. The window exists so the target loan can be swapped if your redemption did not target the lowest-rate loan (this should only happen when something goes wrong on the indexer side). If the swapped-in loan is smaller than your redemption amount, only part of your redemption is fulfilled (at the locked-in price) and the rest of your PUSD is returned to you.

Only mature loans can be swapped in, meaning loans that have already paid interest across multiple periods. A freshly created loan cannot displace the current target, which stops anyone from creating a new low-rate loan to capture a redemption already in progress. New loans can still be the initial target when a redemption first starts.