Borrowing

Last updated: April 8, 2026

Borrowing lets you mint PUSD by depositing BCH as collateral. You keep exposure to BCH price movements while accessing dollar-denominated liquidity.

How borrowing works

- You deposit BCH into a smart contract as collateral

- You choose how much PUSD to mint (up to ~90.9% of the collateral’s USD value)

- You choose an interest rate to pay on your loan

- PUSD is minted to your wallet, and your collateral is locked until you repay

Your loan is represented as an NFT (CashToken) in your wallet. This NFT is your loan key — it proves ownership and lets you manage the loan.

Creating a loan

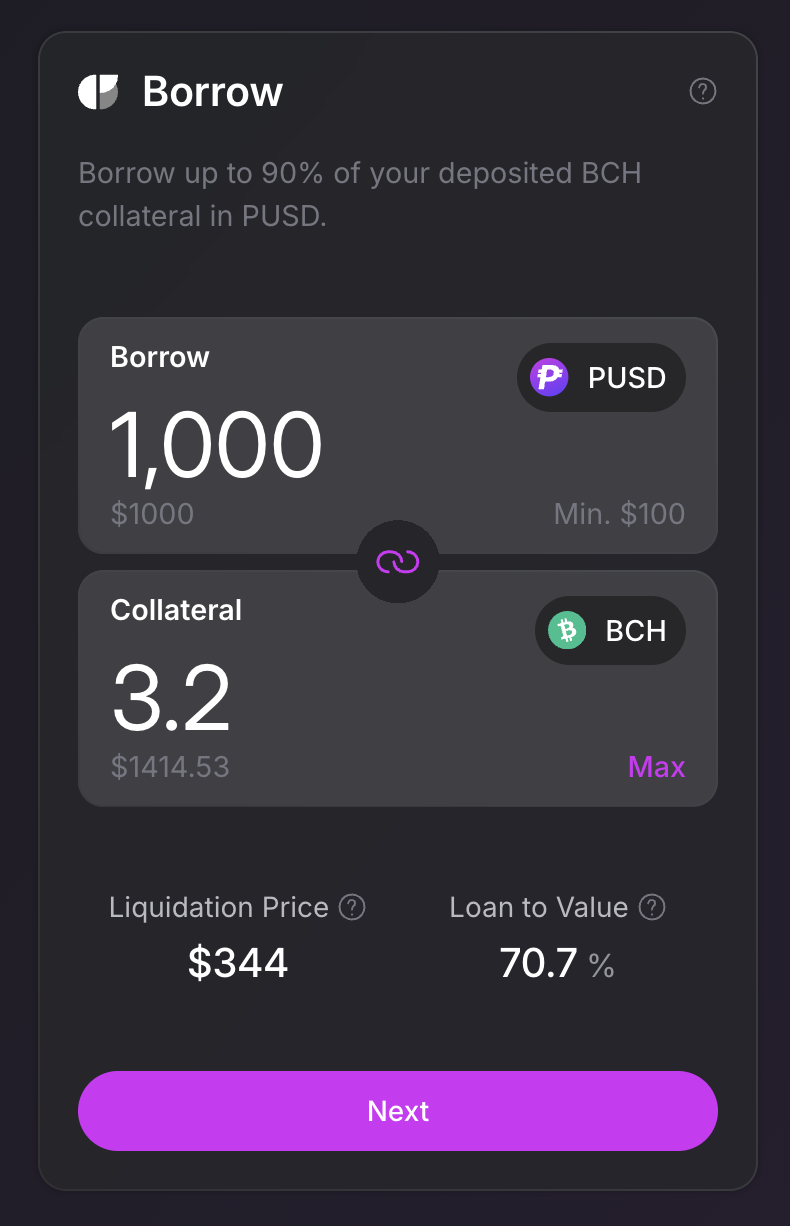

Step 1: Collateral and amount

You need to decide two things:

- How much BCH to deposit as collateral

- How much PUSD to borrow against it

The app shows you two key metrics as you adjust these values:

Loan-to-Value (LTV) — The ratio of your borrowed amount to your collateral’s USD value. Higher LTV means more borrowing but less safety margin.

LTV = Borrowed PUSD / (Collateral BCH × BCH Price)

Liquidation price — The BCH price at which your loan falls below the 110% minimum collateral ratio and can be liquidated. If BCH drops to this price, your collateral is seized.

Liquidation Price = Borrowed PUSD / Collateral BCH × 1.1

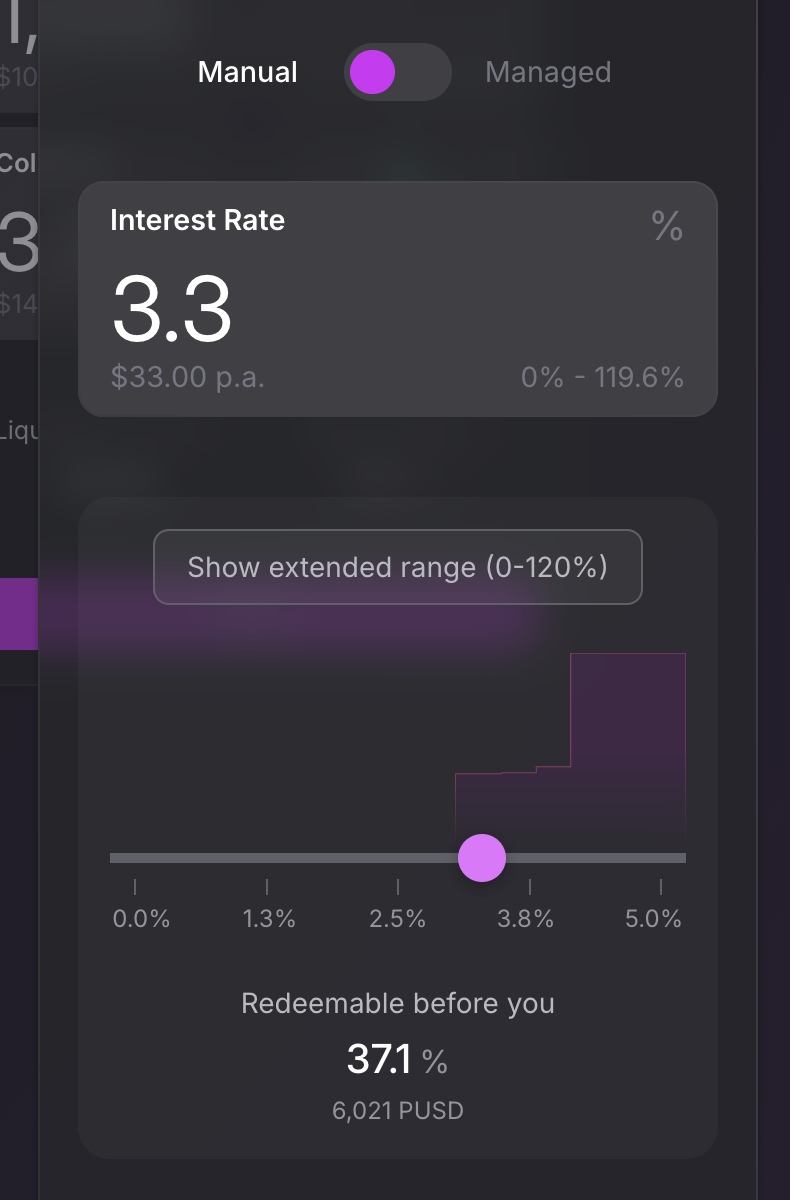

Step 2: Interest rate

You choose your own annual interest rate, from 0% to 119.6% APR (in increments of 0.05%). This is the key tradeoff in ParyonUSD:

- Lower rates are cheaper but leave you more exposed to redemptions. Other users can redeem PUSD against your loan, extracting your BCH collateral at face value.

- Higher rates cost more in interest but protect you from redemptions. The protocol redeems against the lowest-rate loans first, so a higher rate puts you further back in the queue.

You have two options for managing your rate:

Manual rate — You set a fixed rate and adjust it yourself as market conditions change. Best if you want full control.

Managed rate — The protocol’s interest manager automatically adjusts your rate based on a risk strategy you choose (low, medium, or high risk). The interest manager can only adjust your rate — it has no access to your collateral or loan funds. This requires signing two transactions: one to create the loan and one to delegate rate management. You can reclaim control at any time.

Fees

A one-time fee of 0.5% is applied to the borrowed amount when you create a loan:

- 0.25% protocol fee

- 0.25% front-end fee

For example, borrowing 100 PUSD costs 0.50 PUSD in fees. No fees are charged for repaying or managing your loan.

Worked example

Suppose BCH is trading at $500 and you want to borrow PUSD:

| Value | |

|---|---|

| Collateral deposited | 2 BCH ($1,000) |

| PUSD borrowed | 600 PUSD |

| LTV | 600 / 1,000 = 60% |

| Liquidation price | 600 / 2 × 1.1 = $330 |

| Borrowing fee (0.5%) | 3 PUSD |

| Interest rate chosen | 5% APR |

In this example, BCH would need to drop 34% (from $500 to $330) before your loan is at risk of liquidation. A 60% LTV provides a comfortable safety margin.

If you instead borrowed 800 PUSD (80% LTV), your liquidation price would be $440 — only a 12% drop away. Higher borrowing means less room for price fluctuations.

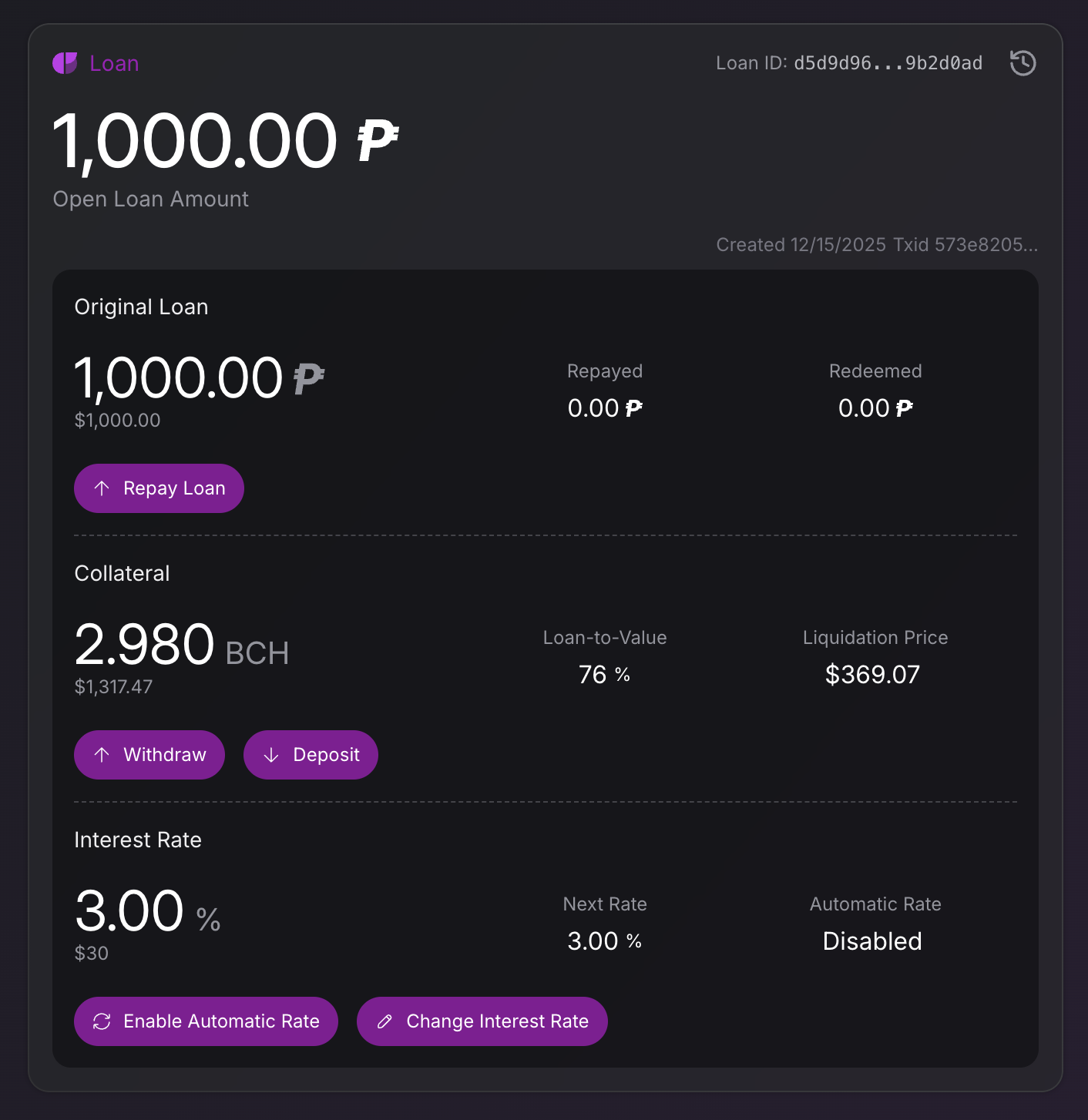

Managing your loan

After creating a loan, you can manage it from the loan detail page:

Repay debt

Pay back some or all of your borrowed PUSD to reduce your debt and improve your collateral ratio. Fully repaying closes the loan and returns all your collateral.

Minimum repayment: ~0.01 PUSD. If partially repaying, at least ~2 PUSD of debt must remain.

Add or withdraw collateral

Add collateral — Deposit more BCH to improve your collateral ratio and lower your liquidation price. Useful when BCH price drops and you want to avoid liquidation.

Withdraw collateral — Remove excess BCH if your loan is well-collateralized. Your collateral ratio must stay above 110% after withdrawal.

Change interest rate

Adjust your rate up or down as market conditions change. If you’re on a managed rate, you can switch to manual (or vice versa) at any time.

Risks

Liquidation

If BCH price drops and your collateral ratio falls below 110%, your loan can be liquidated. Liquidation means:

- Your collateral is seized by the Stability Pool

- Your debt is cancelled

- You keep the PUSD you borrowed, but lose the collateral

How to manage this risk: Keep your LTV well below the maximum. Monitor your liquidation price and add collateral if BCH price is approaching it.

Redemption

Other PUSD holders can redeem their tokens for BCH collateral from the protocol. Redemptions target loans with the lowest interest rates first. If your loan is redeemed against:

- Your BCH collateral is reduced by the amount of BCH sent to the redeemer

- Your PUSD debt is reduced by the corresponding amount

- Your loan remains open with reduced collateral and debt

In dollar terms, the collateral you lose is approximately equal to the debt removed. You don’t lose significant money — but you do lose BCH exposure, which may not be what you want if you’re bullish on BCH. See Redeeming for a worked example.

How to manage this risk: Set a higher interest rate to move further back in the redemption queue. The tradeoff is higher ongoing cost versus better protection.

Interest accrual

Interest is collected periodically (roughly daily) from your collateral in BCH. Over time, this reduces your collateral and worsens your collateral ratio. For long-lived loans with higher rates, monitor your position to ensure interest payments don’t erode your safety margin.